Nasdaq Performs Best During Fed Rate Hikes Since 1994 & Individual Stock News by Sr. Portfolio Manager James R. Wigen -click here-

Since the beginning of 2022 we have seen Stocks drop to levels we have not seen for quite some time.

In my view, some of the reasons the market has dropped is a little overdone. There is no doubt the Fed Funds rate will start to go up soon, how much this year is anyone’s guess, and financial experts on tv, radio, and the internet should not be guessing!

Individual investors are very often influenced by the “financial experts” they listen to on tv, radio or the internet. All I hear lately is how bad Nasdaq stocks are affected when the Fed raises rates. Not so fast!

There is no doubt some Tech stocks trading on the Nasdaq were very much overvalued, however, the “financial experts” recommending to SELL now due to upcoming Fed rate hikes, and how those hikes hurt Nasdaq stocks the most, are factually incorrect, when looking back at data since 1994.

As it turns out, during so-called rate-hike cycles, which could start in March, the market tends to perform STRONGLY, not POORLY.

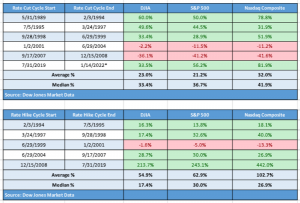

In fact, during a Fed rate-hike period dating back to 1994, provides the following average returns:

Dow Jones Industrial Average DJIA is nearly 55%,

S&P 500 Index a gain of 62.9%,

Nasdaq Composite COMP has averaged a positive return of 102.7%.

This performance was provided by Dow Jones, using data going back to 1994.

Fed interest rate cuts, perhaps unsurprisingly, also yield strong gains:

Dow (DJIA) up 23%,

S&P 500 gaining 21%,

Nasdaq rising 32%, on average during a period of Fed rate cuts.

DKNG – DraftKings

Morgan Stanley analyst Thomas Allen upgraded DraftKings (ticker: DKNG) to an Overweight from Equal Weight. He maintained a $31 price target on the stock in a report titled “Too Big an Opportunity to Ignore; Upgrade to Overweight.”

Based on 21 Wall Street analysts offering 12 month price targets for DraftKings in the last 3 months. The average price target is $43.84 with a high forecast of $76.00 and a low forecast of $23.00. The average price target represents a 126.10% change from the last price of $19.39.

MP – MP Materials

MP Materials finished its first calendar year as a publicly traded company after completing its merger with a special purpose acquisition company, and it was a doozy. Shares of the rare-earth metals miner soared 41% in 2021, according to data from S&P Global Market Intelligence.

In particular, it was the company’s strong performance in the second and third quarters of 2021 that contributed most significantly to its rise. Some positive coverage from Wall Street and a deal with General Motors didn’t hurt, either, in motivating investors to pick up shares.

Legislation Introduced In The Context Of Significant Federal Attention To Vulnerable Supply Chains, Including Critical Minerals And Materials

On January 14, 2022, Senators Tom Cotton (R-AR) and Mark Kelly (D-AZ) introduced the Restoring Essential Energy and Security Holdings Onshore for Rare Earths (“REEShore”) Act “to protect America from the threat of rare-earth element supply disruptions, encourage domestic production of those elements, and reduce [the United States’] reliance on China.” The Senators stated that “[e]nding America’s dependence on the [Chinese Communist Party] for extraction and processing of these elements is critical to winning the strategic competition against China and protecting our national security” and that the REEShore Act “will strengthen America’s position as a global leader in technology by reducing our country’s reliance on adversaries like China for rare earth elements.”

BLNK – Blink Charging

In another noteworthy development, General Motors has joined forces with Blink Charging. Per the pact, Blink Charging would deploy EV chargers at GM dealerships in the United States and Canada, includes around 4,400 dealerships and roughly 10 charging stations per dealership. Working together with leading facility solutions provider ABM, Blink is supplying its IQ 200 Level 2 chargers to the U.S. auto giant. The Blink IQ 200 chargers are the fastest Level 2 AC charging stations available that reduce charge times for new EVs coming to market.

Blink Charging has already shipped chargers to selected GM dealerships in all 50 states across the United States. Currently, it has orders on hand to supply the same in Canada over the next several months.

CHPT – ChargePoint Holdings

The 16 analysts offering 12-month price forecasts for ChargePoint Holdings Inc have a median target of 30.50, with a high estimate of 46.00 and a low estimate of 19.00. The median estimate represents a +165.91% increase from the last price of 11.47.

About ChargePoint

ChargePoint is creating a new fueling network to move people and goods on electricity. Since 2007, ChargePoint has been committed to making it easy for businesses and drivers to go electric with one of the largest EV charging networks and a comprehensive portfolio of charging solutions available today. ChargePoint’s cloud subscription platform and software-defined charging hardware are designed to include options for every charging scenario from home and multifamily to workplace, parking, hospitality, retail and transport fleets of all types.

Today, one ChargePoint account provides access to hundreds-of-thousands of places to charge in North America and Europe. To date, more than 90 million charging sessions have been delivered, with drivers plugging into the ChargePoint network approximately every two seconds.

SOFI – Sofi Technologies – Becoming a Bank

Sofi Technologies has received approval from both the U.S. Office of the Comptroller of the Currency and the U.S. Federal Reserve to officially become a bank holding company. This is major news for SOFI stock. The company has long sought to become an official bank.

Until now, Sofi has had to rely on partnerships with FDIC-insured banks to hold customer deposits and issue loans. The transition to a bank will enable the company to offer a wider array of products beyond the loans, cash accounts and debit cards it already offers to consumers. It will also provide the company with more flexibility to set interest rates and loan terms.

TSLA – Tesla

Tesla reported shortages in Semiconductors, bringing down many EV automakers.

Tesla shares dropped more than 11% in Thursday trading after the company said it would not produce new model vehicles in 2022 — and is not yet working on a hotly anticipated $25,000 electric car.

CEO Elon Musk broke the news to shareholders on a 2021 fourth-quarter earnings call after trading on Wednesday, noting that Tesla is still dealing with chip shortages that are expected to linger throughout the year.

DISCA – Discovery, Inc. / Discovery+

AT&T Tops Q4 Earnings Estimates, WarnerMedia Income Down 38% as Discovery Merger Expected to Close in Q2.

AT&T topped Wall Street estimates for the fourth quarter of 2021, with WarnerMedia revenue gains driving top-line results — helped by strong growth of HBO Max — although the division’s operating income dropped 38% on higher costs.

The company also announced that it expects the WarnerMedia spinoff and merger with Discovery to close in the second quarter (previously, it pegged the close for mid-2022). AT&T said it plans to host a virtual analyst event in the first half of March, providing financial guidance for what the telco’s communications business will look like post-WarnerMedia.

The telco earlier this month pre-announced Q4 results for HBO / HBO Max subscribers, beating its own forecast: The services at year-end tallied 73.8 million combined global subs, up 4.3 million sequentially, over the high end of AT&T’s guidance of 70 million – 73 million.

HBO and HBO Max ended 2021 with 46.8 million U.S. subscribers, a net gain of 1.6 million in Q4 (after a 1.9 million net loss in the prior quarter stemming from the end of Amazon’s HBO distribution deal). Domestic average revenue per HBO/HBO Max subscriber was $11.15 in the quarter, versus ARPU of $11.82 in Q3 2021 and $11.46 in the year-earlier period.

WarnerMedia total revenue grew 15.4% to $9.9 billion, driven by content licensing revenues and strong direct-to-consumer subscription growth, AT&T said. Direct-to-consumer subscription revenue increased by 11.5% year-over-year, to $1.9 billion, but was down sequentially from $2.0 billion in Q3 (a decline AT&T said was due to the termination of the HBO reseller deal with Amazon). Direct costs supporting the DTC business climbed about 44%, to $2.3 billion in Q4 of 2021 versus $1.6 billion in the year-ago quarter.

Overall, WarnerMedia operating expenses in Q4 rose 38%, to $8.3 billion, because of higher film and programming costs and higher marketing spending. The higher expenses included $380 million in DirecTV advertising-revenue sharing costs for inventory sold by WarnerMedia, following AT&T’s spinoff last summer of DirecTV. The segment’s operating income of $1.6 billion was down 37.8% year over year.

The Q4 earnings stand to be one of AT&T’s last to include WarnerMedia, following the $43 billion merger with Discovery in Q2 pending regulatory approvals including by the DOJ.

PENN – Penn National Gaming

This casino operator is expected to post quarterly earnings of $0.46 per share in its upcoming report, which represents a year-over-year change of +557.1%.

Revenues are expected to be $1.51 billion, up 46.9% from the year-ago quarter.

According to the issued ratings of 19 analysts in the last year, the consensus rating for Penn National Gaming stock is Buy based on the current 5 hold ratings and 14 buy ratings for PENN. The average twelve-month price target for Penn National Gaming is $88.12 with a high price target of $142.00 and a low price target of $38.00.

PLUG – Plug Power

Based on 17 Wall Street analysts offering 12 month price targets for Plug Power in the last 3 months. The average price target is $43.71 with a high forecast of $78.00 and a low forecast of $25.00. The average price target represents a 139.38% change from the last price of $18.26.

MSFT – Microsoft

Based on 25 Wall Street analysts offering 12 month price targets for Microsoft in the last 3 months. The average price target is $374.42 with a high forecast of $425.00 and a low forecast of $320.00. The average price target represents a 24.87% change from the last price of $299.84.

PDYPY – Flutter Entertainment – Better Known as Fanduel’s Parent Company

“Separate listing for FanDuel in New York, as planned, would help. Yet it first needs to settle its differences with Fox.”

Flutter and Fox Corp. (NASDAQ:FOXA) are engaged in a now months-long legal spat over the price the latter will pay to buy an 18.6 percent slice of FanDuel. Flutter wants what it believes is fair market value, while Fox wants the price the parent company paid — $4.175 billion in December 2020 — when it bought out investment firm Fastball’s 37.2 percent interest in FanDuel.

Flutter owns 95 percent of FanDuel. Boyd Gaming (NYSE:BYD) owns the other five percent.

Wide Chasm Between Flutter, Fox

Buyers and sellers typically want different prices for an asset. But the gap between what Flutter is willing to sell 18.6 percent of FanDuel to Fox at and what the media company is willing to pay is wide.

As The Sunday Times reports, Flutter wants to sell that portion of FanDuel to Fox at what investment bankers estimated it to be worth in July when sports wagering equities were performing significantly better than they are today.

Potentially further muddying the waters for Fox is that Flutter investors are clamoring for FanDuel to be valued in excess of rival DraftKings (NASDAQ:DKNG). Those two companies are often joined at the hip for investment valuation purposes. But the reality is FanDuel is the largest online sportsbook operator in the US, and holds significantly more market share than its competitor. Even with DraftKings shares shedding nearly 37 percent year-to-date, its market capitalization is $23.64 billion.

The gap between what Flutter will sell the interest at and what Fox will pay is reportedly as large as $10 billion, and it’s the source of the aforementioned legal tussle between the two companies.

In April, Fox confidentially filed a suit against Flutter last week in New York’s Judicial Arbitration and Mediation Services (JAMS). JAMS isn’t a traditional court of law, but its decisions are binding and gives parties a more efficient avenue for settling disputes.

Aiming for Amicable

It’s not clear when a JAMS decision will be reached, nor is it clear when Flutter could commence the FanDuel spin-off. But both sides should be motivated to reach an amicable resolution.

For its part, Fox is also a Flutter investor. It owns 2.5 percent of the gaming company. That relationship stems from Fox selling Sky Bet to The Stars Group (TSG) in 2018 for $4.7 billion. Last year, Flutter shelled out $12.2 billion for TSG,, which, at the time, owned Fox’s FOX Bet unit.

Flutter should want to resolve the matter, too. Because with a FanDuel spinoff, it can unlock shareholder value. That’s while generating capital to firm its balance sheet and pursue other acquisitions to bolster market-leading positions outside the US.

Past performance does not guarantee Future results, therefore, understand investing in the Stock Market can cause you to lose money. Please take the proper risk for your current situation and get the advice from a financial professional who clearly understands your current and future goals and objectives.

All opinions expressed by James Wigen on this website are solely his opinions and do not reflect the opinions of IFP Advisors, LLC, dba Independent Financial Partners, (IFP). Investment Advice offered through IFP Advisors, LLC, dba Independent Financial Partners (IFP), a Registered Investment Adviser. IFP and Wigen Financial Services, LLC are separate entities.

Comments

Leave a Reply

You must be logged in to post a comment.